Saudi Arabia's Consulting Boom : Vision, Transformation, and the New Economic Frontier

Co-written with Mostafa Ali

From Oil Tides to a Diversified Horizon: The Genesis of KSA's Consulting Sector

The early contours of Saudi Arabia's consulting market were largely sculpted by its overwhelming dependence on hydrocarbon wealth. During the era of King Abdullah, advisory services, much like the broader economy, remained "closely tied to fluctuations in oil revenues". Economic activity, including government expenditure, dutifully "followed the price of hydrocarbons". In this climate, the government functioned as "both the primary regulator and client," leading to a cyclical pattern where "Spending on infrastructure, tech, and advisory services would surge during oil booms, only to tighten again when prices fell". This created an inherently unstable demand environment, making sustained growth for advisory services a challenging proposition.

This reliance on oil revenues had a deeper, more structural impact. The immense wealth generated by oil arguably fostered a form of "Dutch Disease," a phenomenon where a significant influx of income from natural resources leads to the weakening of other economic sectors. This extended beyond purely economic symptoms to affect the development of indigenous strategic planning and execution capabilities within governmental and quasi-governmental bodies. The "easy money" effect from resource exports could reduce incentives for economic diversification and weaken economic reforms, as authorities might focus more on distributing rent revenues than developing competitive industries. With less immediate pressure to cultivate diversified economic sectors and the complex management skills they entail, government spending, directly linked to oil income, often prioritized tangible infrastructure projects or wealth distribution over nuanced policy development or organizational transformation. Consequently, when complex advisory needs arose, the default was often to look externally, as internal capacity for such strategic roles had not been systematically nurtured. This created a vacuum that consultancies, predominantly international at the time, were positioned to fill, but it also perpetuated a cycle of external dependency for strategic thought and complex problem-solving.

Within this environment, local consulting firms, particularly "Before 2015, struggled to gain traction". Their limitations were symptomatic of a broader, less developed local business ecosystem. Operating "Without integrated digital tools or strong operational capabilities," these firms functioned at a "limited capacity", unable to compete effectively with the scale and perceived expertise of global players. The boom-bust cycle tied to oil prices further exacerbated their predicament. Unlike large international firms with diversified global revenue streams and substantial financial cushions, local entities found it exceedingly difficult to achieve sustainablegrowth or weather the inevitable downturns in government spending on advisory services. This inherent instability likely deterred investment in local firms, reinforcing the dominance of international consultancies that could absorb such market shocks. Despite the Kingdom having thousands of consulting firms, only a small percentage (around 5%) were locally owned, highlighting this imbalance.

However, even during this period, foundational changes were quietly underway. "King Abdullah’s scholarship programs had sent thousands of Saudis abroad for education". While perhaps not explicitly designed at the time to bolster a nascent consulting sector, this initiative represented significant, long-term strategic investment in national intellectual capital. These programs planted "the seeds of a skilled workforce that would later return to drive transformation", addressing a critical gap in local expertise. The King Abdullah Scholarship Program (KASP), the largest in Saudi history, significantly increased educational opportunities, particularly for women, aligning with broader social reforms and the subsequent Vision 2030's aim to boost female workforce participation. By 2017-2018, women constituted 31% of state scholarship participants studying abroad. The program was restructured over time to align with the Kingdom's changing labor market needs and economic development goals, aiming to benefit the Kingdom from the enhanced education of its populace.6 The exposure of these students to different economic models, advanced business practices, and diverse problem-solving approaches in international academic institutions created a latent potential. Upon their return, these individuals brought not just degrees but new perspectives and a drive to implement change, eventually becoming crucial in staffing new government initiatives, private sector ventures, and, significantly, the burgeoning local consulting firms. Their unique blend of global best practices and an intrinsic understanding of the local Saudi context would, in time, become a formidable competitive advantage.

Vision 2030 : The Great Accelerator of Consulting Demand

The landscape of Saudi Arabia's consulting sector, and indeed its entire economic paradigm, experienced a seismic shift with the advent of Vision 2030. "Everything accelerated after 2017 with the launch of Vision 2030," a comprehensive blueprint "spearheaded by Crown Prince Mohammed bin Salman," which "laid out a bold path toward economic diversification and modernization". This was not merely a new set of policies; it represented a fundamental re-imagining of the Saudi economy, a strategic pivot away from oil dependency towards a diversified, knowledge-based future, aiming to increase the private sector's GDP contribution to 65% by 2030. The sheer ambition of this vision inherently created an unprecedented and sustained demand for strategic advice, sophisticated planning, and robust implementation support across a multitude of sectors. The Kingdom's spending on consulting services surged significantly, with some estimates indicating a 17.5% increase to nearly €2 billion annually compared to 2022, making Saudi Arabia a colossal client for firms like BCG.

This marked a fundamental departure from a historically reactive economic management style, which primarily responded to oil price fluctuations, to a proactive, strategic nation-building endeavor. Such a profound transformation necessitates a completely different scale and typology of consulting services one focused on creating entirely new industries, reforming governance structures, driving societal change, and fostering innovation, rather than merely optimizing existing operations or managing cyclical infrastructure spending. This shift has engendered a sustained, high-level demand for consulting that, while not entirely immune to broader economic conditions (overall GCC consulting market growth is expected to slow slightly from 13.3% in 2024 to 12% in 2025, reaching $8.3 billion), is significantly less susceptible to the short-term volatility of oil prices. The Saudi consulting market itself saw growth of 38% in 2022 and 25% in 2023, with a projected 13% for 2025.

Central to this national overhaul is the Public Investment Fund (PIF), which has become "a pillar of this shift". Wielding "over SAR 2.6 trillion in assets" (managing assets worth US$930 billion as of early 2025), the PIF has aggressively "poured investments into new sectors tourism, entertainment, sports, infrastructure and birthed mega-projects like NEOM". Giga-projects such as NEOM, Red Sea Global (formerly The Red Sea Project), Qiddiya, Roshn, and Diriyah are central to this strategy. NEOM, a $500 billion city, and other large-scale developments like the $15 billion AlUla cultural project and the King Salman Park, the world's largest urban park, create immense opportunities for consulting firms. The colossal scale of PIF's investments planning to increase the private sector's share of GDP to 65% by 2030 and focusing on 13 key industry sectors and the novelty of many of these target sectors for the Kingdom meant that deep consulting expertise became indispensable. These "ambitious ventures demanded robust advisory support" for a wide spectrum of needs, including feasibility studies, market entry strategies, "operational design, digital architecture, and execution". The PIF aims to increase its and its subsidiaries' contribution to local content to 60% by 2025 through its "Musaama" program.

The PIF's role extends far beyond that of a conventional investor; it acts as an "ecosystem creator". By initiating mega-projects (14 giga projects in total) and seeding new industries, it generates concentric circles of economic activity and, consequently, demand for consulting services. Each new PIF-backed entity or project, such as NEOM (a planned $1.5 trillion development), Qiddiya entertainment city, or the Roshn residential developments, becomes a nucleus. This generates initial consulting demand for master planning (Qiddiya Investment Company collaborated with Bjarke Ingels Group for its master plan), financial modeling, and infrastructure design for the primary project. Subsequently, secondary demand arises from hotels, transport companies, entertainment providers (Saudi Entertainment Ventures, a Qiddiya company, plans a $13 billion investment in 21 entertainment attractions), and myriad service industries seeking to operate within or support these new destinations. Further, tertiary demand emerges from regulatory bodies overseeing these new activities, workforce development agencies training the necessary human capital, and marketing firms branding these new ecosystems. The PIF is also actively partnering with international firms to accelerate growth and transfer technology and knowledge, such as its MoU with Goldman Sachs Asset Management to anchor new private credit and public equity funds focused on Saudi Arabia and the GCC.

The impact of Vision 2030 is evident in the broadening scope of advisory needs. Previously, "Tourism was largely confined to pilgrimage". Today, "the transformation is visible everywhere: cultural agencies organize festivals and performances; sports committees form around football, skydiving, and squash; infrastructure projects accelerate as Saudi Arabia prepares to host the World Cup and other global events". Saudi Arabia's hosting of the 2034 FIFA World Cup is set to further boost infrastructure and consulting spend. Each of these burgeoning areas "urban planning, entertainment, and environmental rehabilitation" requires specialized consulting support, signifying a maturing and diversifying market for advisory services. This includes a significant push towards sustainability, with a $266 billion investment planned for green initiatives, aiming for 50% renewable energy by 2030, creating demand for clean energy advisory services.

A critical driver for this heightened consulting demand is the "implementation imperative" embedded within Vision 2030. The vision is not merely a collection of aspirational goals; it is accompanied by aggressive timelines and an unwavering focus on execution. Before the current transformation, the government "managed a massive portfolio of initiatives but lacked structures for tracking outcomes". The establishment of Vision Realization Offices (VROs) within ministries such as the Ministry of Health's VRO for the Healthcare Transformation Strategy, and a general focus on transformation governance bodies (including PMOs, TMOs, and VROs) highlight this shift. Surveys show that a significant portion of transformation programs (60%) focus on internal optimization, business process optimization (22%), and technology/digital adoption (20%) to achieve organizational goals and align with national metrics. This historical context underscore the vital need for consultancies that can not only advise but also actively support project management, build capabilities within government agencies, and oversee the rollout of complex, multi-stakeholder initiatives. This has led to longer, more embedded consulting engagements focused on delivering tangible results.

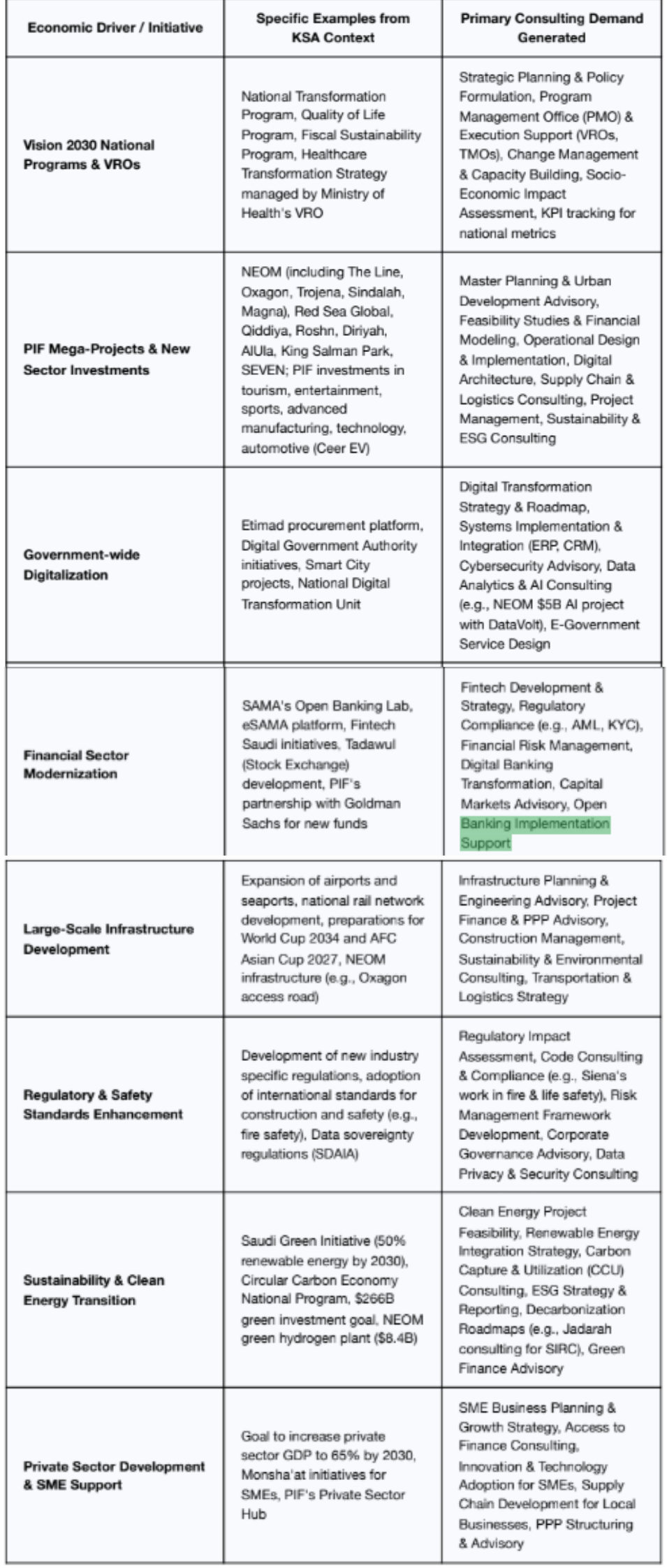

The following table summarizes the key economic drivers under Vision 2030 and the corresponding demand generated for consulting services:

Table 1 : Key Economic Drivers and Resulting Consulting Demand in KSA Post-Vision 2030

Digitalization and Financial Modernization: Carving New Consulting Niches

Parallel to the grand-scale diversification efforts under Vision 2030, targeted government initiatives in digitalization and financial sector reform have acted as potent catalysts, forging entirely new and specialized markets for consulting services. These reforms are not merely internal administrative improvements; they are fundamentally reshaping how both government and the private sector operate, thereby generating specific and often urgent advisory needs. The digital transformation consulting services market in Saudi Arabia was valued at $1.4 billion in 2023 and is anticipated to grow at a CAGR of 23.5% through 2029, while the broader digital transformation market is expected to reach nearly $70 billion by 2030 with a CAGR of 30.9% from 2025.

A cornerstone of this modernization drive has been "the digitalization of government processes," recognized as a "key milestone" in the Kingdom's transformation agenda. A prime exemplar is "Etimad, the Ministry of Finance’s unified procurement platform," which has effectively "streamlined tenders, contracts, and payments". This platform aims to increase transparency in governmental tenders, enhance spending efficiency, and boost SME participation. By 2025, Etimad had processed over 32 million transactions with a 96% digital rate and an 85% use satisfaction rate. This initiative has done more than enhance efficiency; it has pushed "government agencies and private sector players to adopt standardized, transparent workflows". The mandatory shift to such digital platforms created an immediate and substantial demand for consulting services in areas like business process reengineering, technology selection and implementation (especially in cloud computing, data analytics, cybersecurity, and AI), robust change management programs, and extensive training modules for public and private sector entities alike as they adapted to these new sophisticated systems. This government-led push for digitalization acts as a powerful forcing function, compelling greater transparency, standardization, and efficiency across the public sector and its manifold interactions with private enterprises. The ripple effect extends to private companies, which are now compelled to upgrade their own systems and processes to interface effectively with these new governmental digital infrastructures, thereby creating further consulting demand for their own internal transformations and compliance adjustments.

Simultaneously, "the Saudi Central Bank (SAMA) advanced the financial ecosystem with platforms like eSAMA and the Open Banking Lab". SAMA launched its Open Banking Framework in November 2022 and the Open Banking Lab in January 2023, with a focus on Payment Initiation Services (PIS) in early 2024. These strategic moves have "modernized the sector and opened space for consulting firms to support fintech development, compliance, and strategy". Open banking allows third-party providers to access financial data with customer consent, enabling innovative solutions like personalized financial products and seamless payment systems. This has spurred the growth of fintech apps and platforms like Tarabut Gateway, Drahim.sa, and Spare, which leverage open banking APIs. This is a clear illustration of how proactive policymaking can directly cultivate new, high-value consulting niches. SAMA's initiatives are not merely about enhancing the financial sector in isolation; they are critical enablers of the broader economic diversification goals. A modern, agile, and increasingly open financial system is indispensable for supporting the growth of new industries particularly fintech, small and medium-sized enterprises (SMEs), and innovative startups all of which are central to Vision 2030. This, in turn, fuels demand for specialized financial, regulatory, and technology consulting to help new fintechs navigate the evolving regulatory landscape (including robust data security and cyber risk management), for incumbent banks to adapt their models, and for businesses across sectors to leverage new financial tools and platforms.

The sheer scale and pace of digital transformation in core government functions are vividly illustrated by the overhaul of the budgeting process. "Until 2017, agencies managed their budgets with outdated spreadsheets and paper records". In a remarkably short period, a radical shift has occurred: "Now, more than 220 entities are expected to submit digitalized budgets by October each year". This represents "a radical shift requiring comprehensive training, implementation, and coordination under intense time pressure". Such a "compressed transformation," implementing profound systemic changes across a vast number of organizations against tight deadlines, creates an acute, short-to-medium-term surge in demand for consultants. These consultants must possess the capabilities to manage large-scale, complex projects, deliver results swiftly, and often navigate environments requiring skills in crisis management and rapid deployment. The success of this ambitious digitalization drives significantly on the effective and timely deployment of such specialized consulting resources. The healthcare sector, for example, has seen investments of almost $15 billion in ICT infrastructure since the establishment of a National Digital Transformation Unit, with a focus on telemedicine, EHRs, and AI to improve efficiency and accessibility.

The Ascendance of Local Expertise: Reshaping the Competitive Landscape

As Saudi Arabia's economy has matured and its strategic priorities have sharpened under Vision 2030, the competitive dynamics within its consulting market have undergone a significant realignment. This shift has seen the challenges faced by previously dominant international consultancies grow, while simultaneously charting the rise of local firms, increasingly led by Saudi professionals equipped with international experience and a nuanced understanding of the Kingdom's unique context. By 2022, foreign firms had nearly monopolized the Saudi consultancy market.

"Early on, global giants like Accenture and PwC dominated" the Saudi consulting scene, alongside other major players like McKinsey, BCG, Deloitte, and EY. However, as the market evolved and client expectations became more sophisticated, "challenges quickly surfaced". Among the primary sticking points were "Cultural mismatches, high fees, and imported strategies that didn’t adapt to local realities". These issues often led to suboptimal outcomes or implementation difficulties, with criticisms including questionable advice, shallow presentations, and even "copy-paste consulting" where deliverables for other countries were reused. The economic rationale for a shift became particularly compelling when considering cost structures; for instance, "international firms often billed director-level consultants at 250,000 SAR per month while local talent could deliver similar outcomes for a fraction of the cost". This stark differential, coupled with a growing desire for solutions more attuned to the Saudi environment, began to erode the unchallenged dominance of global players. Incidents such as the reported year-long ban on PwC from new PIF advisory work in early 2025, though not publicly explained, signaled increasing scrutiny and a reassessment of foreign consultant involvement, with a stronger focus on measurable returns and cost containment. Concerns over data sovereignty, with stricter regulations being drafted for data handling by firms involved in sensitive sectors, also played a role.

This evolving landscape has paved the way for local consulting firms. "In this maturing market, local consulting firms have begun to gain ground". A key characteristic of this new wave of domestic consultancies is that "Many are led by professionals with global experience, especially in defense, healthcare, and public sector transformation". This signifies a critical development: the emergence of a credible and capable local alternative. These firms often combine international best practices and methodologies with a deep, intrinsic understanding of local business culture, bureaucratic nuances, and the overarching strategic objectives of Vision 2030. This "contextual intelligence" is increasingly being valued by clients over generic international frameworks that may lack the necessary adaptability. The rise of these firms is not merely about offering lower costs; it represents a redefinition of the value proposition itself, emphasizing project management and business practices tailored to Saudi culture and regulations.

The earlier, far-sighted investment in human capital through initiatives like King Abdullah's scholarship programs is now directly fueling the competitiveness of these local firms. The thousands of Saudis educated and often professionally seasoned abroad are not just returning as employees; many are the founders and leaders of these new local consultancies. They bring with them credibility, international networks, modern skill sets, and an ambition to contribute directly to their nation's development. This is a direct and tangible payoff from a long-term human capital strategy, elevating the overall quality and capability of the local consulting ecosystem and making it a more viable and often preferred alternative to relying solely on international firms. This, in turn, reduces dependency on imported talent and fosters the growth of an indigenous professional services industry. Government "Saudization" policies, such as mandating 40% Saudization in consulting firms, 35% in engineering consultancy, and 30% in financial advisory, aim to create high value jobs for Saudis and ensure they are well trained. These policies are expected to create over 8,000 high-value jobs and retain $1.2 billion annually in the economy.

Furthermore, the maturation of the Saudi market is evidenced by the emergence of specialized local firms catering to niche demands. "Specialized firms have also emerged to support regulatory compliance and risk management". A prominent example is "Siena, a prominent example, operates across MENA and has been pivotal in promoting fire and life safety engineering in Saudi Arabia". Their specific expertise in "code consulting, safety assessments, and fire protection ensures that new infrastructure adheres to international standards a growing necessity as the country urbanizes and scales up construction". Similarly, local firms like Jadarah Business Consulting are active in specialized areas like decarbonization strategy, assisting clients like the Saudi Investment Recycling Company (SIRC). In the early stages of a market's development, demand often gravitates towards generalist strategy and management consulting. However, as an economy and its constituent projects become more complex exemplified by Saudi Arabia's massive infrastructure buildout and the development of new, highly regulated industries the demand for highly specialized, technical expertise naturally grows. This fosters the development of niche players, indicating a more sophisticated, segmented, and mature consulting landscape capable of addressing highly specific challenges. Government initiatives like those by the Local Content and Government Procurement Authority (LCGPA), which promotes the "Made in Saudi" initiative and aims to increase local content in government procurement, further support this trend. The PIF's local content policy, "Musaama," aims for 60% local content from PIF and its subsidiaries by 2025. Additionally, Monsha'at, the General Authority for Small and Medium Enterprises, provides support including remote consulting services to entrepreneurs and SMEs in fields like finance, technology, and law. Aramco's In Kingdom Total Value Add (IKTVA) program also plays a crucial role in driving supply-chain efficiency and encouraging the development of a diverse, globally competitive energy sector, with a goal to retain 70% of all procurement spend in-Kingdom and a special focus on SMEs.

Market Dynamics and Future Outlook : Navigating Opportunities in a Transformed Kingdom

The Saudi consulting market is poised for continued robust growth, driven by the sustained momentum of Vision 2030 and the Kingdom's unwavering commitment to economic diversification and modernization. The market reached $4.3 billion in 2024 and is expected to grow by 13% in 2025, making it the largest and fastest growing in the Gulf, though growth is slightly moderating from the post-Covid exponential surge. The dynamics of shaping this market are multifaceted, reflecting both the vast opportunities and the evolving expectations for advisory services.

Demand for consulting support remains indispensable and is projected to be particularly strong across sectors central to Vision 2030. These include "urban planning, entertainment, and environmental rehabilitation", which are undergoing transformative development. Alongside these, ongoing and accelerated needs in large-scale infrastructure development (especially with the Kingdom preparing to host global events like the World Cup 2034 and AFC Asian Cup 2027), tourism expansion, the burgeoning sports ecosystem, and the pervasive drive for digital transformation across all government and private sector entities will continue to be major consumers of consulting services. The digital transformation consulting market alone is projected for a CAGR of 23.5% through 2029. Demand for ESG (Environmental, Social, and Governance) consulting is also rising as Saudi Arabia aims for net-zero emissions by 2060 and implements initiatives like the Saudi Green Initiative. The healthcare consulting market is also expanding due to privatization efforts (aiming for 35% private sector involvement by 2030), digital health advancements ($1.5B+ invested), and regulatory reforms under the Health Sector Transformation Program. Similarly, the education sector sees active involvement from both global firms like BCG and local specialists like Emkan Education and Jadarah. The nature of this demand will span the entire consulting value chain, from high-level strategic formulation and policy advice to intricate project management, specialized technical expertise, and hands-on execution support.

While the ascent of local firms is a defining feature of the current market, "Saudi Arabia is also actively supporting foreign firms entering the market". However, this support is strategically calibrated. The Kingdom recognizes that "Regulations, licensing, and market access can be complex" for international entities.1 In response, initiatives are in place "to provide advisory support and representatives on the ground". This facilitation is not an unconditional open-door, but part of a curated approach designed to leverage global expertise strategically. For instance, the Regional Headquarters (RHQ) Program, announced in 2021, encourages multinational corporations to establish their regional HQs in Saudi Arabia to be eligible for public tenders from January 1, 2024. The overarching goal is clear: "attract high-quality players, ensure alignment with national priorities, and embed long-term value in every partnership". This implies a preference for foreign firms that can bring truly differentiated expertise, contribute to local capability building (a critique of past engagements was the failure to embed long-term expertise), and demonstrate a clear commitment to the Kingdom's long-term development objectives.

The future competitive landscape is unlikely to witness a complete displacement of international firms. Instead, a "coopetition" model – blending cooperation and competition is emerging. International consultancies possessing highly specialized global knowledge, proprietary technologies, or the sheer capacity to manage mega-projects at an immense scale may still find significant opportunities. However, their mode of operation will need to adapt. There will be increasing pressure and expectation to partner with local firms, transfer knowledge effectively, and demonstrably contribute to the development of Saudi talent. The government's explicit emphasis on embedding "long-term value" and achieving "real knowledge transfer" strongly suggests a preference for partnerships that build sustainable local capabilities rather than perpetuating a dependency on external providers. Clients are becoming more selective, pushing for value over volume, and questioning cost structures and expected outcomes, leading to more aggressive pricing and thinner margins, especially on large public sector contracts.

Beyond physical infrastructure and new industry creation, consulting services are becoming increasingly crucial for the development of Saudi Arabia's "soft infrastructure." This encompasses the establishment and refinement of regulatory frameworks, the enhancement of institutional capacity within government bodies, the cultivation of talent development ecosystems, and the fostering of innovation hubs. The documented need to effectively manage complex portfolios of initiatives, rigorously track outcomes, and implement sophisticated systems like digital budgeting across numerous entities are prime examples of building this essential institutional muscle. Initiatives like the Misk Foundation's Career Essentials Program, which has benefited over 700,000 young Saudis by preparing them for the job market with essential soft skills and career guidance, and its various leadership and entrepreneurship programs, contribute significantly to talent development. The Human Resources Development Fund (HRDF) also plays a role by supporting training, employment programs, and offering loans to training institutions. In these endeavors, consultants often act as catalysts, temporary capacity builders, and facilitators of complex change management processes.

The role of the Saudi government itself is evolving significantly. While it remains a primary, and often the largest, client for consulting services, its function is expanding to that of a strategic shaper of the consulting market. Through procurement policies that increasingly favor local content (e.g., LCGPA regulations giving preference to Saudi individuals, establishments, and products) or local partnerships, targeted support for SMEs (which includes many emerging local consultancies via Monsha'at and IKTVA's focus), and the clear conditions placed on foreign firms regarding alignment with national priorities and value embedding, the government is actively cultivating a consulting ecosystem that serves its long-term national interests. This represents a more sophisticated, and at times interventionist, approach to market development, aimed at ensuring that the billions spent on advisory services yield maximum economic and developmental returns for the Kingdom.

Final Thought: A New Chapter for Consulting in the Kingdom

The consulting sector in Saudi Arabia has navigated a remarkable journey, transitioning from a peripheral service tied to the fortunes of oil to a central enabler of an ambitious national reinvention. The impetus provided by Vision 2030, coupled with substantial investments spearheaded by the Public Investment Fund and a government-wide mandate for digitalization and modernization, has fundamentally reshaped demand, creating a multi-billion dollar market characterized by both scale and increasing sophistication, projected to exceed $4.8 billion in 2025.

Key economic transformations, including the strategic diversification away from hydrocarbons, the digitalization of state functions exemplified by platforms like Etimad and the modernized budgeting systems, and the modernization of the financial sector through SAMA's Open Banking initiatives, have not only broadened the scope of consulting needs but have also deepened the requirement for specialized expertise. This has spurred growth in areas ranging from strategic planning and PMO support for giga projects like NEOM to niche advisory in fintech development, cybersecurity, ESG strategy, and regulatory compliance. The market is maturing, with clients becoming more cost-conscious and demanding measurable impact.

A defining characteristic of this new era is the confident emergence of local consulting firms. Bolstered by a growing cadre of Saudi professionals educated and experienced internationally a legacy, in part, of programs like King Abdullah's scholarships and supported by Saudization policies and local content initiatives, these firms are increasingly competing on value, offering contextual understanding and cost-effectiveness that challenges the traditional dominance of global players. The rise of specialized entities like Siena and Jadarah further underscores the market's maturation.

Looking ahead, the Saudi consulting market is set for sustained expansion, albeit with evolving competitive dynamics. The government's role will continue to be pivotal, not just as the principal client but as a strategic architect of the market, encouraging partnerships that embed long-term value, foster knowledge transfer, and align with national priorities. For both local and international players, success will increasingly depend on their ability to deliver tangible outcomes, cultivate local talent through programs like those offered by Misk Foundation and HRDF, and navigate a landscape where deep sectoral knowledge, specialization, and an understanding of the Kingdom's unique transformational journey are paramount. The story of consulting in Saudi Arabia is no longer just about providing advice; it is about actively participating in the construction of a new economic frontier, demanding greater accountability, local impact, and true partnership.

Sources :

Interview with Strategy Development and Excecution Expert Mostafa Ali

KSA Vision 2030 Excecution member